Venture Capital's Red Velvet Ropes Are Coming Down

The most valuable companies in the world are private. For the first time, you can invest in them. Sort of.

If you have worked in the startup ecosystem, at some point, a friend or relative has asked you the same question: “how do I invest in startups?”

Your answer is usually vague, as you know how closely guarded the gates of venture capital are. In an industry where success is defined by access and network, it has been virtually impossible for a well-off retail investor to invest in a breakout startup.

But change is in the air in 2026. The velvet ropes of venture capital are coming down. Well, somewhat.

A New Kind of Access

Last week, VCX by Fundrise, a $650 million venture capital fund made a splashing debut on Wall Street.

Retail investors poured in capital like it was some golden ticket to wealth creation. Why? A closer look at the fund’s holdings will spell out the answer for you:

Assets that, until now, were effectively off-limits unless you were writing eight-figure checks or sitting inside a top-tier fund.

It was the first time that ordinary investors had access to buying a piece of the hottest private technology companies like Anthropic and OpenAI. And this stock gave you proxy access to three foundational AI labs, the world’s leader in autonomous defense systems and private market leaders in payroll, gaming and compliance.

Robinhood’s Decade-Long Bet

Robinhood, the fintech giant, also listed its own $658 million venture capital fund in February, allowing retail investors to participate in tech unicorns.

Robinhood's entry into this space matters more than the product itself. Vlad Tenev (Robinhood CEO) has spent a decade taking financial products that were once restricted and making them accessible: options, crypto, fractional shares.

The 2021 GameStop episode nearly broke the company and the pretense that keeping retail investors out was for their own good.

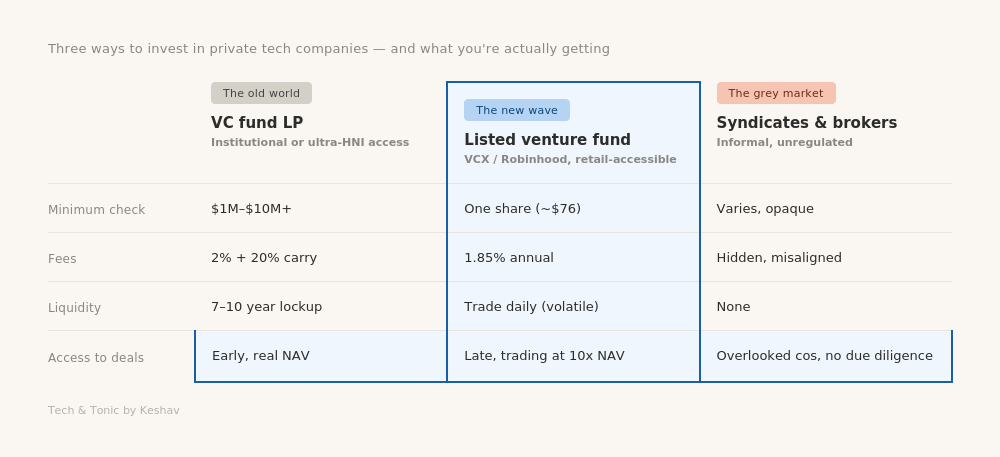

Robinhood Ventures Fund I is not perfect, it excludes the marquee names like SpaceX and Anthropic, trades on secondaries with no redemption rights, and its prospectus openly admits there will be "uncertainty as to the value of its portfolio investments."

But, none of that diminishes what they are actually doing: normalizing the idea that private markets should be accessible, and forcing the rest of the industry to respond. The product is version one and will evolve, it is the principle that counts.

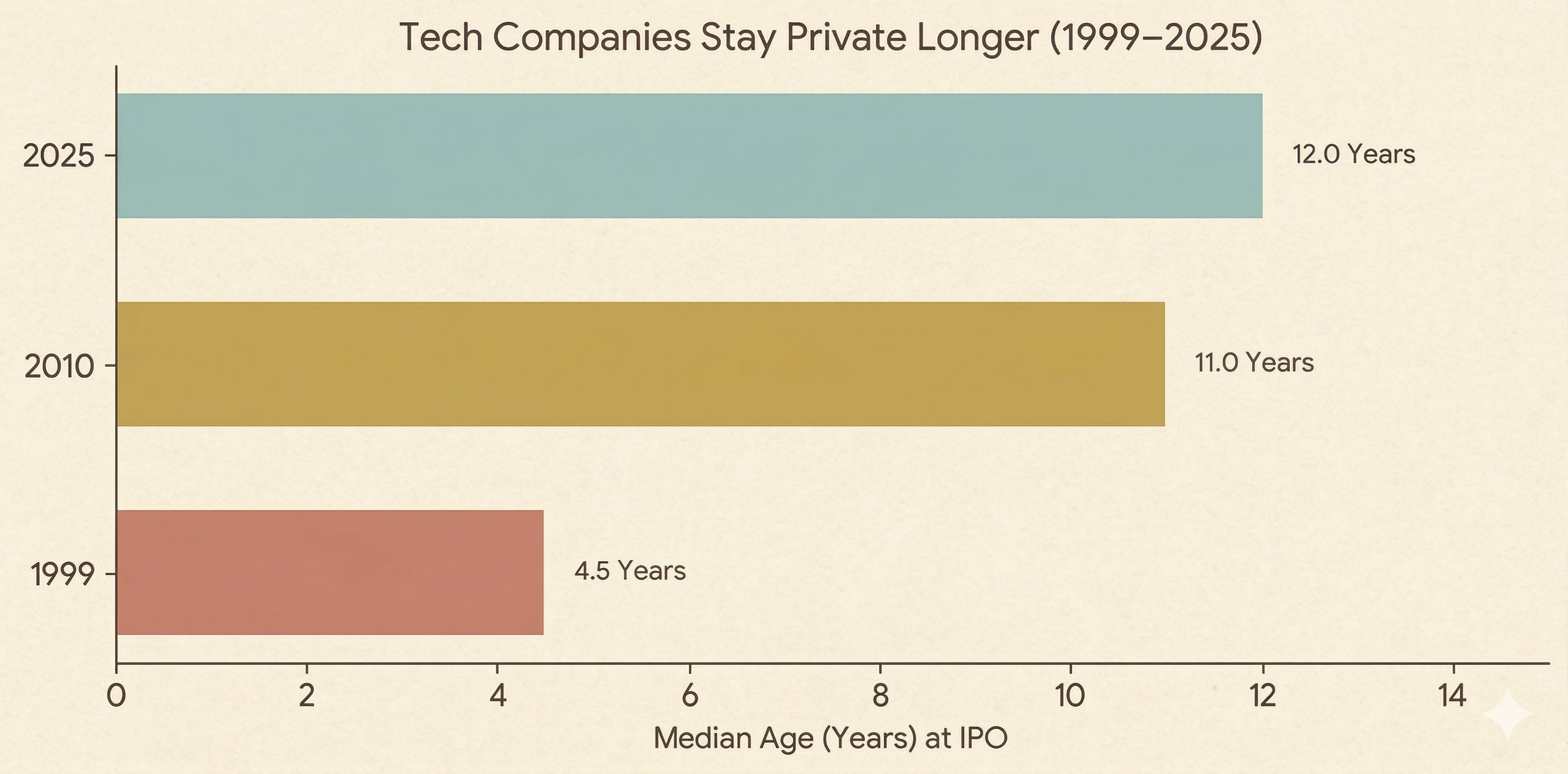

The Best Companies Stay Private

Today, some of the most valuable new companies in the world are private. OpenAI, SpaceX, Anthropic, Stripe. The old model of “companies go public when they grow up” has collapsed as more mature companies are staying private longer, compounding in value longer, and distributing those returns exclusively to institutional investors and their networks.

By the time they IPO (if they do), much of the upside is already captured.

Retail investors have been sitting out the best decade in technology wealth creation by design.

These funds are the first serious crack in that wall.

The fine print is messy

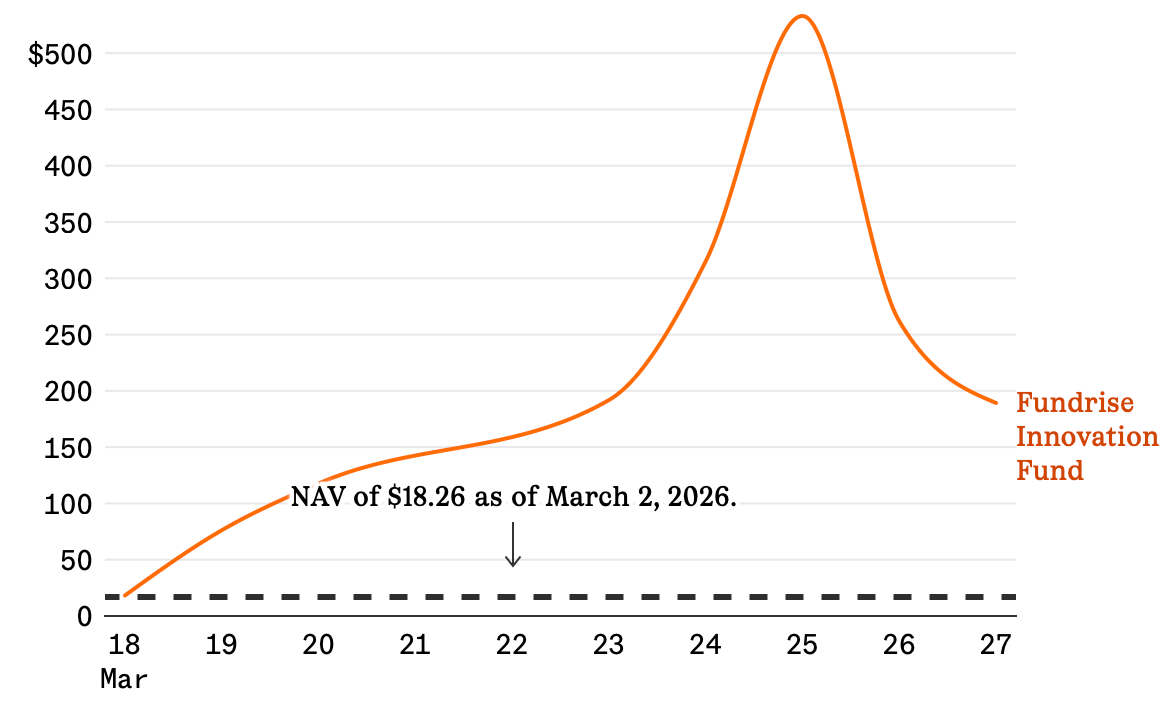

Fundrise’s stock opened to the public at $76 a share. It peaked at $533 but by end of the week, it had crashed to $189. Buried in the IPO paperwork is a little detail: “You should purchase shares of the fund only if you can afford a complete loss of your investment.” But, the underlying portfolio is genuinely strong.

The problem is what happens when retail hunger for AI exposure meets a fixed supply of shares - you get meme stock behavior wrapped in a venture capital label.

When Anthropic and SpaceX eventually go public, their stocks will likely soar, but not enough to justify buying them today at 20x their estimated private market value, inside a 1.85% annual fee wrapper.

This is what version one of democratization looks like: real access, real upside for early movers, and real danger for those who confuse the wrapper for the asset.

The velvet rope came down last week. The room behind it is still being built.

The Access Was Always the Point

Venture Capital’s traditional model was designed to keep a specific kind of capital compounding for a specific kind of investor. The argument has always been that retail investors needed protecting from illiquid, high-risk assets. VCs and their LPs got rich on asymmetric access. Everyone else got to read about it afterward.

The veil of secrecy around venture capital served insiders and it is right that it is lifting. The first products are overpriced, fee-heavy, and carry disclaimers that should give serious pause. But soon enough, the market will mature and better-structured products will follow. The product will improve because the demand is real, right from the by-lanes of Mumbai to local cafés in New York, everyone wants a piece of these high-growth, elusive businesses.

A Thought for India

Many Indian families with high disposable income have long wanted to invest in startups and diversify beyond their traditional assets like gold, stocks and PMS schemes.

But instead of structured access, there are grey markets and syndicates. Brokers who would offer to ‘get you in’ on a supposedly ‘hot’ company (read: BlueSmart) which was overlooked by many institutional investors for the right reasons. Opaque deals follow with misaligned incentives.

If this model works in the US, India will follow, after all it is the third largest startup ecosystem. The risk is copying without building the guardrails. A listed fund holding private Indian tech companies is no longer a radical idea. It is an overdue one.

For years, the honest answer to “how do I invest in startups” was: well, you can’t, not really. That answer is getting harder to give now. The industry I work in is losing one of its oldest walls, and I think that’s right.

The rope is coming down.