The SaaS Panic is Misreading the Power Shift

Who Captures Value in the Age of AI

Every few years, markets decide an industry is finished. Retail was supposed to die when Amazon scaled and Media was supposed to die when social platforms took distribution.

Five years later, Walmart runs a thriving digital business and The New York Times has over 10 million subscribers.

Technological shifts rarely erase entire categories. However, they do reorganize who captures value within them.

Now it’s software’s turn.

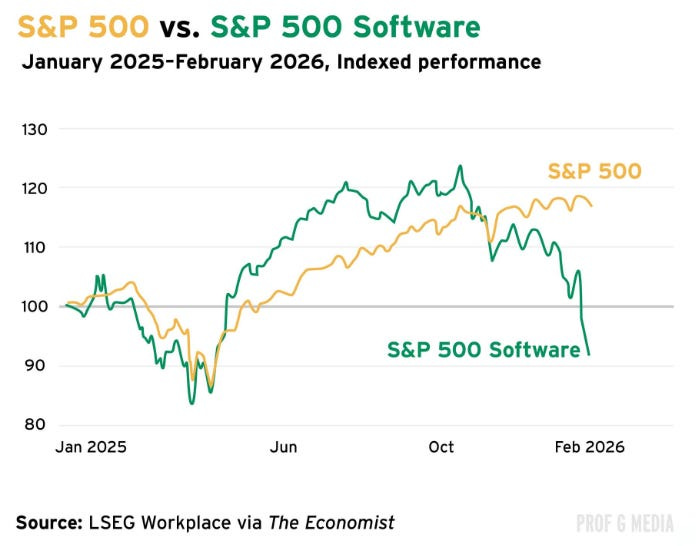

Nearly $800 billion has been wiped out of software stocks in 2026. Salesforce is down 28% while HubSpot is down 51%. The prevailing thesis is simple: AI agents will kill SaaS. Why would a company pay for Salesforce when its engineers can vibe-code a CRM over a weekend?

That conclusion rests on a misunderstanding of where power sits in enterprise software.

I spent three weeks obsessing over SaaS economics and the impact on the industry’s long term outlook. In this piece, I argue that the SaaS-o-calypse is overrated:

When features commoditize, distribution becomes the moat.

Systems of record often become invisible infrastructure.

AI agents depend on the data layer they claim to disrupt.

Productivity expansion is more likely than zero-sum destruction.

Not every SaaS company will be impacted in the same way, some will thrive.

Markets are pricing death where margin compression is the more likely outcome.

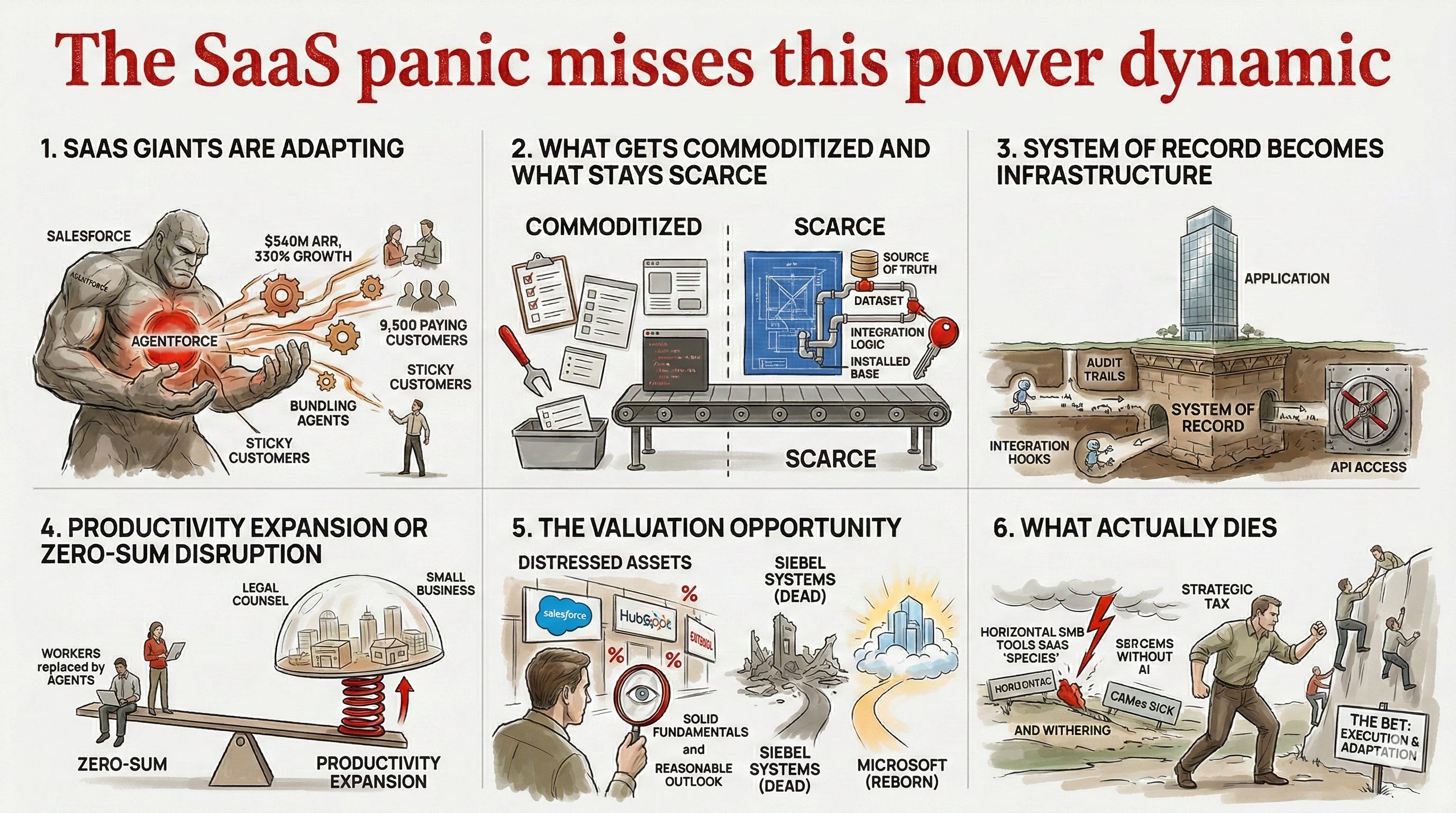

SaaS Giants are Adapting

If AI agents were truly displacing systems of record, the impact would already be visible in demand.

Instead, Salesforce posted its best quarter yet and just launched their fastest-growing product in its history. Agentforce reached $550 million in ARR within months, growing at 330% and serving more than 9,500 paying customers.

The bear case assumes incumbents will not be able to compete with AI-native startups. However, a software giant like Salesforce has 150,000 customers and even ServiceNow has 8,400 customers. These are large, sticky customers with years of workflow data and the ability to bundle agents within existing contracts.

If anyone can build a great sales agent, the advantage goes to someone who already has a customer relationship.

What gets commoditized and What stays scarce

AI eliminates feature-based moats and amplifies distribution based moats.

UI, workflows, features are all surface functionality that can be replicated easily with AI and are now commoditized.

But systems of record are the dataset of how a business operates with custom fields that encode institutional knowledge. Integration logic connects the CRM with billing, marketing, finance and support functions. It is the source of truth for an organization, deeply embedded in all functions.

Installed base, years of sales and pipeline data, integration hooks into different systems become valuable in large organizations.

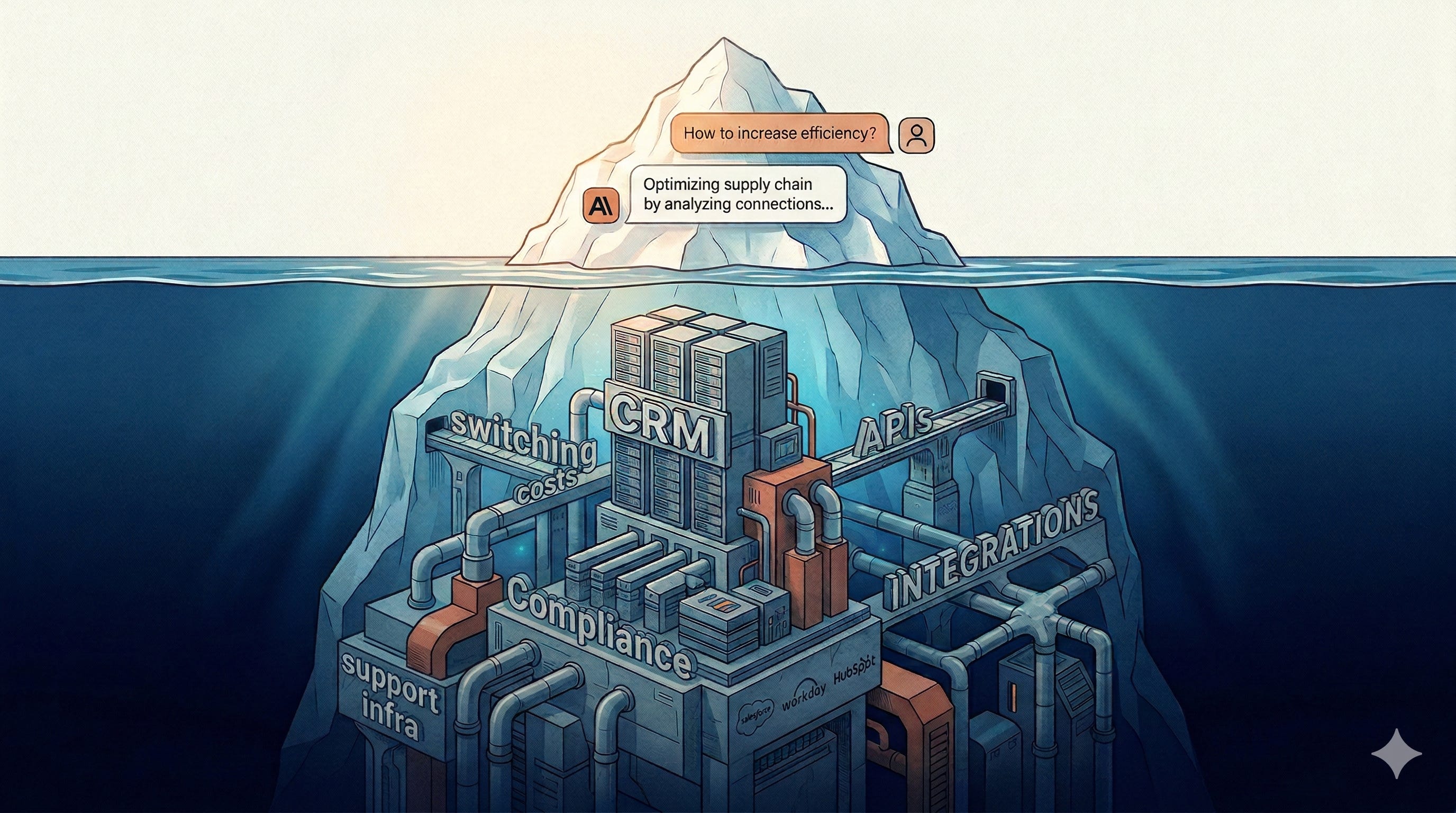

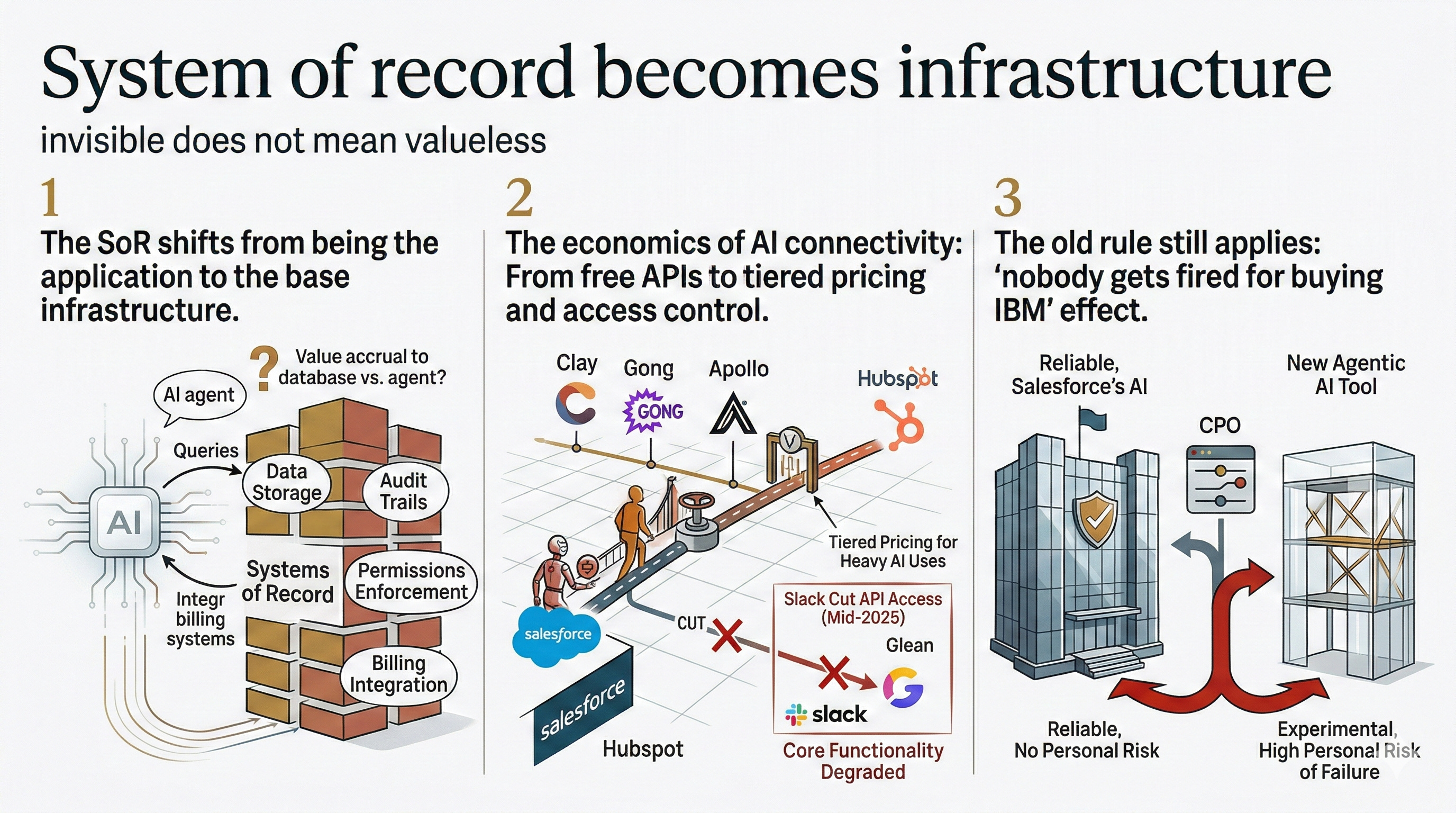

System of record becomes infrastructure

What will happen to systems of record once AI Agents start generating leads, managing pipelines, and even closing deals? Won’t the CRMs become invisible?

Yes. But, invisible does not mean valueless:

Instead of sales reps logging into Salesforce, agents will query it. And these agents will need a place to store data, maintain audit trails, enforce permissions, and integrate with billing systems. The SoR shifts from being the application to the base infrastructure.

The bigger question is how much value do you accrue to the database of leads versus the agent who generates them?

All AI tools like Clay, Gong, Apollo integrate with Salesforce or Hubspot. The APIs are free right now, but that won’t be the case forever.

When Salesforce launches tiered pricing for heavy AI uses, what will happen to the economic viability of agents?

In fact, when Slack cut API access to Glean in mid-2025, it severely impacted Glean’s core functionality. Because Glean was blocked from storing and indexing long term data from slack, it materially degraded its functionality and usability.

The old rule still applies: “nobody gets fired for buying IBM” effect. If you are the CPO of a large public company and you put in a new Agentic AI tool and it fails, you are in big trouble. If you went with Salesforce’s AI and it fails, nobody blames you.

Jenson Huang frames it simply: if we achieve AGI, does AI reinvent a new tool or use an existing one? The tools are designed to be used. An AGI does not need to rebuild SAP or ServiceNow from scratch, it would simply use them.

Productivity Expansion or Zero-Sum Disruption

The bear case, highlighted in the Citrini piece, assumes that the impact of AI will be zero sum - agents replace workers, companies invest more in AI to defend margins and the cycle further decelerates downward.

That is not how technology shifts work. When the cost to produce something falls dramatically, the demand expands significantly as well. If legal services become 70% cheaper, more small business can afford legal counsel. Productivity gains get transmitted via lower prices and expand markets, they do not just compress margins.

The Valuation Opportunity

Salesforce trades at 4.5x sales while growing Agentforce 330%. HubSpot is down 58% despite 20% revenue growth and a record $54 million GAAP profit. These platforms are being valued as distressed assets despite solid fundamentals and reasonable outlook.

Will margins compress? Probably, yes. But there is a massive difference between ‘margins compressing by 20%’ and ‘software is dead’.

Microsoft faced an existential threat when cloud computing emerged. Their entire revenue which was built on Windows revenue was at risk and the stock markets dismissed them.

But Microsoft transformed and turned Azure into a $100 billion business. They went from being purely software-dependent to dominating cloud infrastructure.

Siebel was the dominant CRM before Salesforce which died when cloud happened. The stock market doesn’t know yet who becomes Microsoft and who will become Siebel Systems.

Right now, the market is pricing every software business as Siebel, and therein lies the opportunity.

What actually dies

Not all SaaS companies will survive, the bear case has merit in specific areas. Horizontal SMB tools with low switching costs face genuine risk. CRMs do face the risk of becoming low-margin data stores if they do not adapt and develop new Agentic capabilities embedded in workflows.

However, AI might actually collapse the switching costs. If the migration time drops from 12 months to 3 months, incumbent defensibility will erode quickly. Klarna replaced Salesforce and Workday with internal tools, showing that seat compression is a real challenge.

But 3 months is still a quarter of disruption. The real question is whether AI reduces risk enough to overcome organizational inertia and executive career risk. Many Fortune 500 enterprises will not take that bet.

And on seat compression: yes, some customers will need fewer seats but productivity expansion will matter more. CRMs will lose a few seats per customer but might gain more customers overall. That is business model evolution.

Incumbents face what Brett Taylor (ex-Salesforce co-CEO, and chairman of OpenAI) calls the ‘strategy tax’ where their strengths (resources, large teams, order books) become weaknesses. Public companies can’t let revenues fall off a cliff in a bid to transform their practices, which is where a 50 person startup has an inherent advantage. The difference between the companies that die and those that transform is the willingness to take hard leadership calls.

But explaining yourself to Wall Street isn’t the same as lacking the ability to adapt. Satya Nadella proved it at Microsoft and Marc Benioff is proving it now with AgentForce.

The Bet

AI Agents will create enormous value and some SaaS companies will die. AI is radically transforming software engineering as 4% of all GitHub commits are generated by Claude Code. A similar transformation is now coming for SaaS.

Incumbents with data, distribution and resources have inherent structural advantages which they can leverage to bundle AI into existing contracts. Pricing models will have to shift towards outcome-based usage and pricing to compete with agile startups. The technology landscape is shifting rapidly and the companies that pay the strategy tax and still execute will survive. Microsoft proved it. Someone in the SaaS boat will prove it again.

The market sees Siebel Systems everywhere, but I see a few companies becoming Microsoft. That gap is the opportunity.

Sources and further reading: