Your Thumb Is the New Box Office

Plot twist every 90 seconds. Free until episode 10. Then it’s decision time: wait or pay. From Jaipur to Manhattan, micro-dramas are rewriting entertainment economics

Priya, a 34 year old housewife in Jaipur, discovered Chai Shots through a friend who watches it during her daily train commute in Mumbai. Now, between household chores and her afternoon breaks, Priya finds herself watching 30 to 40 minutes at a stretch, sometimes more.

She’s not alone. In China, 270 million people watch micro-dramas daily on apps like Kuaishou. In India, startups have raised $45 million to chase the same model. In the US, apps like ReelShort generated $1.3 billion in revenue last year, the highest of any market outside China.

These dramas are full length movie plots with CEO revenge fantasies, secret billionaire romances, family betrayals that are chopped into 60 to 90 second episodes. Each one ends on a cliffhanger. The first 10 episodes are free. Then you pay.

And millions of people do.

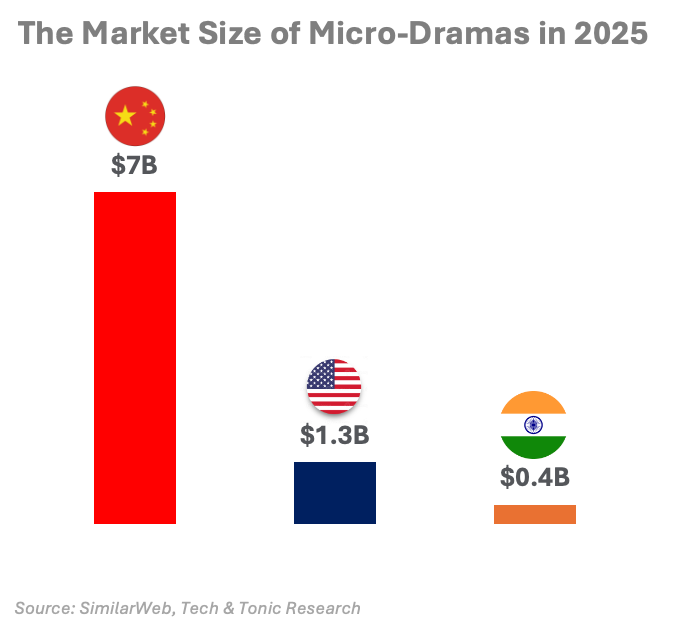

This is the micro-drama revolution: an $11 billion global industry that’s rewriting the rules of entertainment economics. But here’s what everyone covering this trend is missing: the format is global, but the playbook isn’t.

What works in China had to adapt for India. And what’s succeeding in Manhattan is transforming again in Mumbai.

I spent the last few weeks researching this industry across three markets, talking to users, trying the apps myself, and analyzing the business models. What I found reveals something deeper than just “short attention spans.” It’s a story about payment infrastructure, cultural psychology, and why the same format requires radically different execution in each market.

The Chinese Blueprint: How to Monetize Addiction

Let’s start with the numbers that made investors pay attention.

Kuaishou, one of China’s leading micro-drama platforms, has:

270 million daily active users.

Of those, 94 million binge watch more than 10 episodes a day, up 50% from last year.

China’s micro-drama market is now bigger than the country’s entire box office, worth $7 billion!

The top 10 micro-drama apps in China generated $1.7 billion in 2024, with about half of that coming from international markets.

But the real innovation lies hidden in the business model.

I tried ReelShort myself to understand the hook. Within minutes, I was three episodes deep into “The Double Life of My Billionaire Husband.” The production quality was... let’s call it functional. But the pacing was surgical. Each episode ended exactly when my curiosity peaked. Episode four loaded automatically. Then five. Then six.

At episode 10, the screen went black. A notification popped up: “Unlock the next episode for $0.10.”

I was hooked. And I wasn’t alone, this series has nearly 500 million views!

Streaming giants burn millions creating prestige TV. Kuaishou makes money off your curiosity.

Traditional streaming operates on fixed costs. Whether you watch one hour or 100 hours of Netflix, you pay $15.99. Micro-dramas invert this. The more you watch, the more you pay. Your addiction becomes their revenue stream.

The production costs make it possible. A full-length movie, 2-3 hours of content split into 90-second episodes, costs between $150,000 to $300,000 to produce in China. Compare that to Netflix’s $200 million budget for “Rebel Moon.” One show has 200 million views. The other has 2 billion. Guess which one is profitable.

This only works because of micropayment infrastructure.

In China, WeChat Pay made 10-cent transactions frictionless. You don’t think about paying 10 cents. It’s not a decision; it’s a reflex. The friction between “I want to know what happens next” and “I just paid for it” disappears.

That infrastructure and the rails that enable tiny, instant payments, is what makes the entire business model possible.

And it’s completely different in every market.

India’s Adaptation: Audio-First and Freemium

India’s micro-drama story started differently.

When Pocket FM and Kuku FM launched audio-based serialized content, they weren’t copying China’s video model. They were solving for India’s unique conditions: inexpensive mobile data, multitasking culture during commutes, and regional language preference.

Audio worked. Pocket FM raised $103 million and reportedly generates over $150 million in revenue. The content isn’t CEO fantasies, it is built on family drama, regional mythology, and romance told in Hindi, Tamil, Telugu, and other languages.

Then came the video wave. Flick TV, Chai Shots, Quick TV, and others raised $45 million combined, in the last 12 months, to bring China’s model to India’s 900 million internet users.

Priya, the housewife in Jaipur, represents their target demographic perfectly. She watches during her breaks: while waiting for lunch to cook, during her afternoon rest, sometimes late at night after the kids are asleep. Her friend in Mumbai watches during her 90-minute train commute. Both discovered the apps through word of mouth, not advertising.

India’s has a particular advantage over China, and especially over the US. UPI. India’s Unified Payments Interface has made micropayments as seamless as WeChat Pay in China. A ₹10 recharge (10 coins) takes seconds. There’s no minimum transaction fee eating into margins. The payment infrastructure enables the business model.

But here India diverges from China. Indians will pay, but not enough to cover costs alone.

A micro-drama costs $150,000 to $300,000 to produce in China. In India, startups claim they can produce content for “less than 5% of the cost of a video OTT series” or roughly $50,000 to $100,000 per title, with a 28-30 day production cycle.

Still, the math requires creativity.

Indian digital ad rates are far lower than China or the US. Apps cannot survive on ads alone. But subscription and micropayment revenue in a market where users are price-sensitive won’t cover costs either. At least not yet.

The answer? Layered monetization. Freemium models (10-20 free episodes to hook users), micropayments for individual episodes, monthly subscriptions, AND brand-integrated storytelling. Some startups are even experimenting with brands sponsoring entire plot arcs.

It’s working. The industry is projected to reach $5 billion in India within five years. Apps are scaling to $10M+ annual revenues in months. But it’s a fundamentally different playbook than China, where micropayments alone sustain the industry.

The American Evolution: Same Format, Different Infrastructure

Now let’s talk about the US. And why it’s becoming the most interesting market to watch.

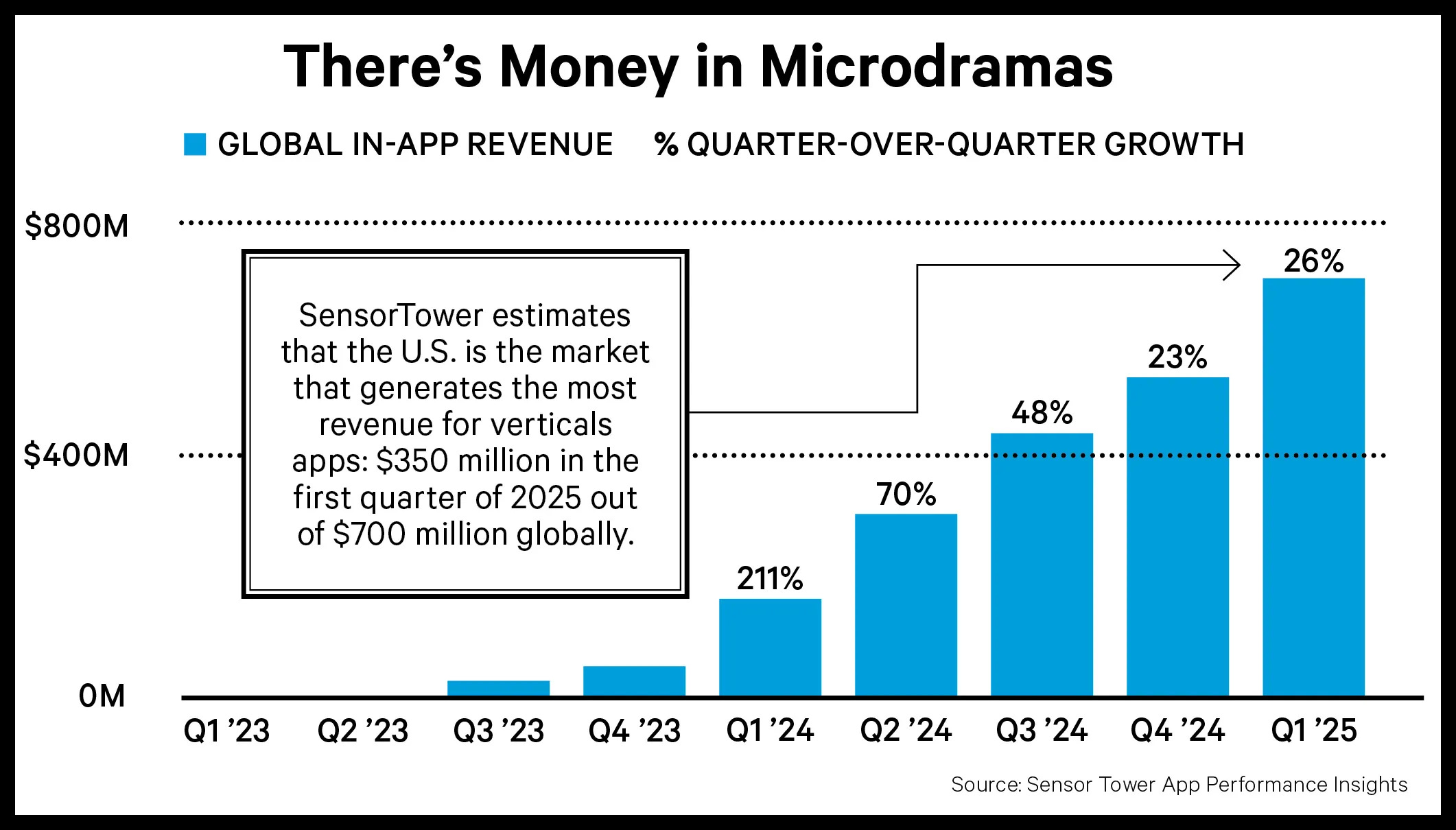

The numbers are staggering. The US leads the international micro-drama market with $1.3 billion in revenue in 2024, more than any other country outside China. In Q3 2024 alone, micro-dramas globally generated $800 million, having doubled from $400 million year-over-year.

The top 20 apps reach 250 million monthly active users, about 10% of US mobile users. Nearly half (46%) of viewers are aged 18-34. ReelShort’s most popular title has almost 500 million views.

Apps are spending heavily on growth: 68% of total US micro-drama ad spending came from social media: Facebook (25%), TikTok (19%), Snapchat (16%), and Instagram (8%).

This is explosive growth.

What makes the US market fascinating: it’s succeeding despite fundamentally different conditions than Asia. And that’s forcing innovation.

The Infrastructure Challenge:

The US doesn’t have seamless micropayment rails like WeChat Pay or UPI. Credit card processing fees make 10-cent transactions unprofitable. So US apps are adapting.

Most now offer multiple payment options:

Coin purchases (buy in bulk, spend per episode, amortizing transaction costs)

Monthly subscriptions (unlimited access, familiar model)

Ad-supported viewing (watch an ad to unlock an episode)

It’s not as elegant as China’s pay-per-episode model, but it’s working. The infrastructure constraints are forcing better product-market fit for American consumer behavior.

The Consumption Behavior Reality

I thought Americans didn’t have the “pockets of time” that make micro-dramas work in Asia. But the data proves otherwise. 250 million monthly active users aren’t wrong.

What’s different is when and why they watch.

In China and India, micro-dramas fill commute time and waiting periods, captive moments with nothing else to do. In the US, people watch during different gaps: lunch breaks, before bed, while waiting for kids at pickup, during boring moments at home.

Americans aren’t watching during train commutes (most drive). But they’re finding their own micro-moments. The format works. The timing is just different.

The Competition Landscape

The US has TikTok, YouTube, Netflix, Disney+, HBO Max, cable TV, and sports all competing for attention.

And they’re succeeding by offering something none of those platforms provide: serialized, scripted storytelling designed for mobile consumption with immediate gratification.

TikTok is raw. Netflix demands time. YouTube is too varied. Micro-dramas occupy the sweet spot: professional content, minimal commitment, maximum addictiveness.

The Production Model Innovation

This is where the US might actually lead innovation. In a recent interview, one L.A. based producer who’s gone full-time into micro-dramas mentioned that he produces one series per month, working across 12 different verticals with various studios and apps. His budgets range from $150,000 to $300,000.

But he’s pioneering a new production model:

Non-union talent (for now)

Writers trained specifically for 90-second narrative arcs

Directors who understand mobile-first pacing

Rapid production cycles (28-30 days from concept to launch)

It’s a completely different system than traditional Hollywood or streaming. And it’s creating a new category of entertainment professionals who understand this format natively.

The Evolution Path

I think we’ll see:

Platform Integration - TikTok, YouTube, Instagram testing their own serialized content (leveraging existing user bases and payment systems)

Celebrity/Influencer Entry - Once Mr. Beast or Emma Chamberlain create a micro-drama series, the floodgates open. Parasocial relationships + serialized content = massive opportunity

Premium Tier Emergence - Some creators will push production quality higher, targeting the gap between current micro-dramas and traditional streaming

Interactive Formats - Choose-your-own-adventure micro-dramas where payment unlocks different story paths

Vertical Integration - Successful apps will start producing their own content, controlling both distribution and production (like Netflix did with streaming)

The US market is growing 100% year-over-year not by copying Asia, but by adapting the format to American infrastructure, behavior, and expectations.

What This Really Reveals: Formats Travel, Models Don’t

Here’s the meta-lesson that matters beyond micro-dramas:

Content formats can go global. Business models do not, at least not without radical adaptation.

Everyone talks about the “global internet” and “universal content.” But entertainment economics are stubbornly local. They depend on:

Payment infrastructure (UPI in India, WeChat Pay in China, credit cards in US)

Competitive landscape (what else is available?)

Consumption behavior (commutes, idle time, cultural habits)

Production costs (labor, regulations, unions)

Willingness to pay (micropayments vs subscriptions vs ads)

Micro-dramas work in China because of seamless micropayments, long commutes, and cheap production. They’re adapting in India through layered monetization and even lower costs. They’re transforming in the US through hybrid payment models, different consumption patterns, and quality differentiation.

Same format. Three playbooks. All working.

The Future: Three Paths, One Direction

So where does this go?

In China: Continued dominance and innovation. Expect AI-generated content to reduce production costs further, interactive storytelling formats, and expansion into adjacent categories (education, fitness, news). The infrastructure and behavior patterns are locked in.

In India: The next 24 months will separate winners from losers. Success will go to whoever cracks sustainable unit economics through brand partnerships and tiered monetization. Regional language content will drive differentiation.

In the US: Platform integration and creator-led content will define the next phase. Standalone apps like ReelShort are proving the market. But long-term, I expect this format to get absorbed into TikTok, YouTube, and Instagram—the same way Stories went from Snapchat to everywhere.

My take: the biggest winner might not be in entertainment at all.

The real innovation here is monetizing attention in 90-second increments through perfectly engineered addiction loops.

Once you perfect that, the cliffhanger mechanics, the friction-free payments, the dopamine triggers, you can apply it to anything.

Imagine Duolingo lessons structured like micro-dramas. Peloton workouts that end on cliffhangers. Financial literacy courses that make you pay to unlock the next lesson. Recipe apps where you unlock cooking steps one at a time.

The formula is dopamine hits powered with micro-payments. That’s what makes this $11 billion industry so much more important than it looks.

The Takeaway

Priya in Jaipur will keep watching Chai Shots during her afternoon breaks. Her friend in Mumbai will keep watching during her train commute. 250 million Americans will keep unlocking episodes during their lunch breaks and late-night scrolling sessions.

And each market will keep evolving the playbook to fit their reality.

But here’s what I’m sure of: the future of entertainment is local.

The most successful content companies of the next decade won’t be the ones who create one global format and force it everywhere. They’ll be the ones who understand that infrastructure, behavior, and economics differ in every market, and adapt accordingly.

The Micro-Drama trend is not a copy-paste across geographies. In India, that means freemium plus brand integration. In America, that means hybrid payment models and platform integration. In China, it means AI-generated content and interactive formats.

Because in the end, your thumb decides what’s worth watching. And it doesn’t swipe the same way in Jaipur, Manhattan, and Shanghai.

Same format. Three futures. All thriving.

What’s one format you think works globally, but needs a local business model to thrive? Hit reply or drop a comment - I’d love to hear your take.

Thanks for reading Tech & Tonic. If you enjoyed this deep dive, subscribe for weekly analysis on how companies work when systems collide. Next week: How Formula 1 went from elitist sport to cultural phenomenon.

Dumbing down of content will make people lazy

Very interesting read! Thanks for the deep dive.