The Most Powerful People in AI Aren't Who You Think

The crypto miners, data center prophets, and high school dropouts who control the $611 billion backbone of artificial intelligence

The AI boom looks like a software story. It isn’t.

It’s an infrastructure buildout on a scale we haven’t seen in decades, consuming land, power, and capital faster than markets can adjust. While the wider attention stays fixed on models and chips, the biggest fortunes are being made elsewhere: in data centers, electricity, and the systems that move data.

That’s where this story begins.

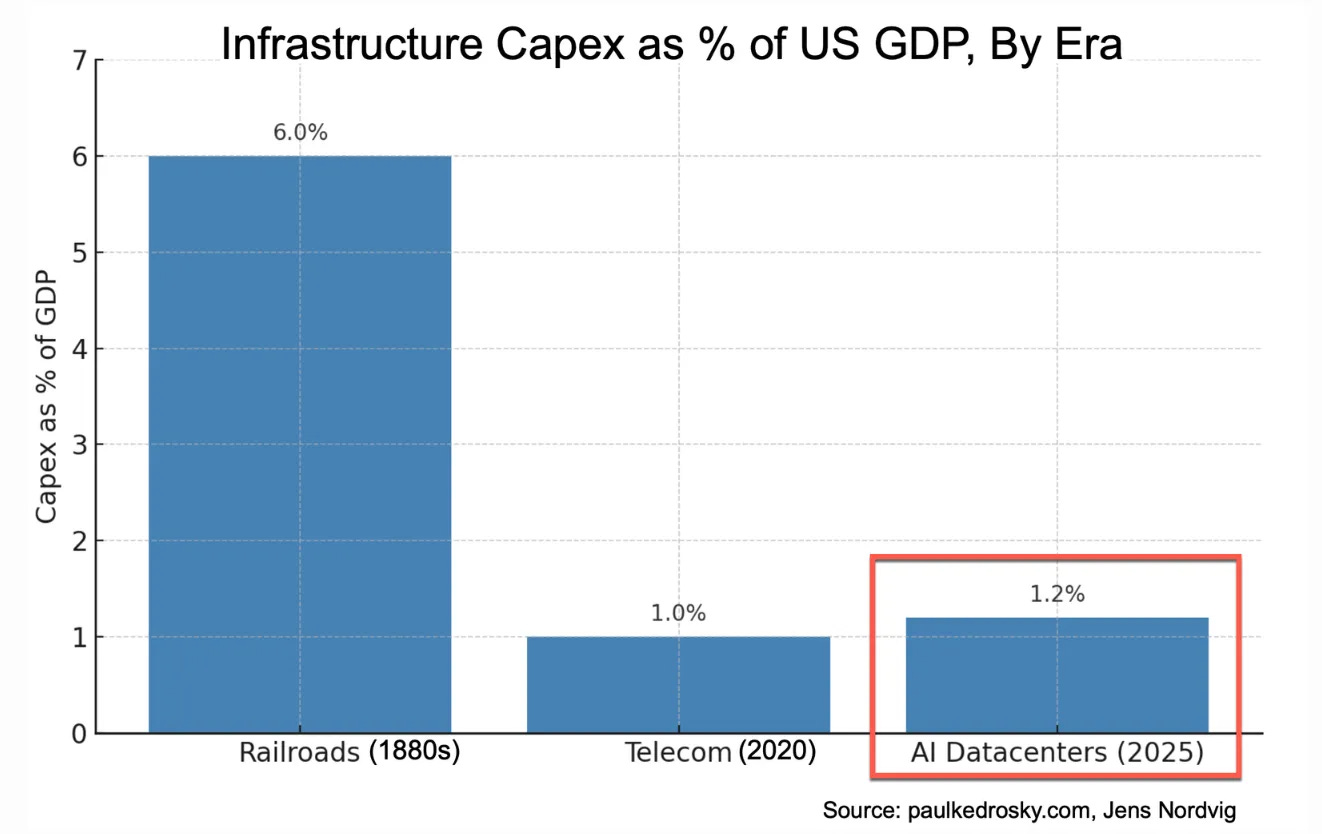

“Artificial intelligence is consuming capital faster than investors can recalibrate,” reported Bank of America recently. Global hyperscale spending is projected to rise 67% in 2025 and another 31% in 2026, with total outlays climbing to $611 billion. This level of spending is already pushing capital intensity far beyond historical norms.

Data centers have been the cornerstone powering intelligence and compute since the era of modern computing began. But the vast capacity needed for the artificial intelligence boom has resulted in a sudden wave of investment into the once-sleepy industry. Here again, the companies that provide the picks and shovels - real estate, electricity generation, and connectivity, are the ones making the most money. NVIDIA is still the apex predator, but the second-order winners are where the story gets interesting.

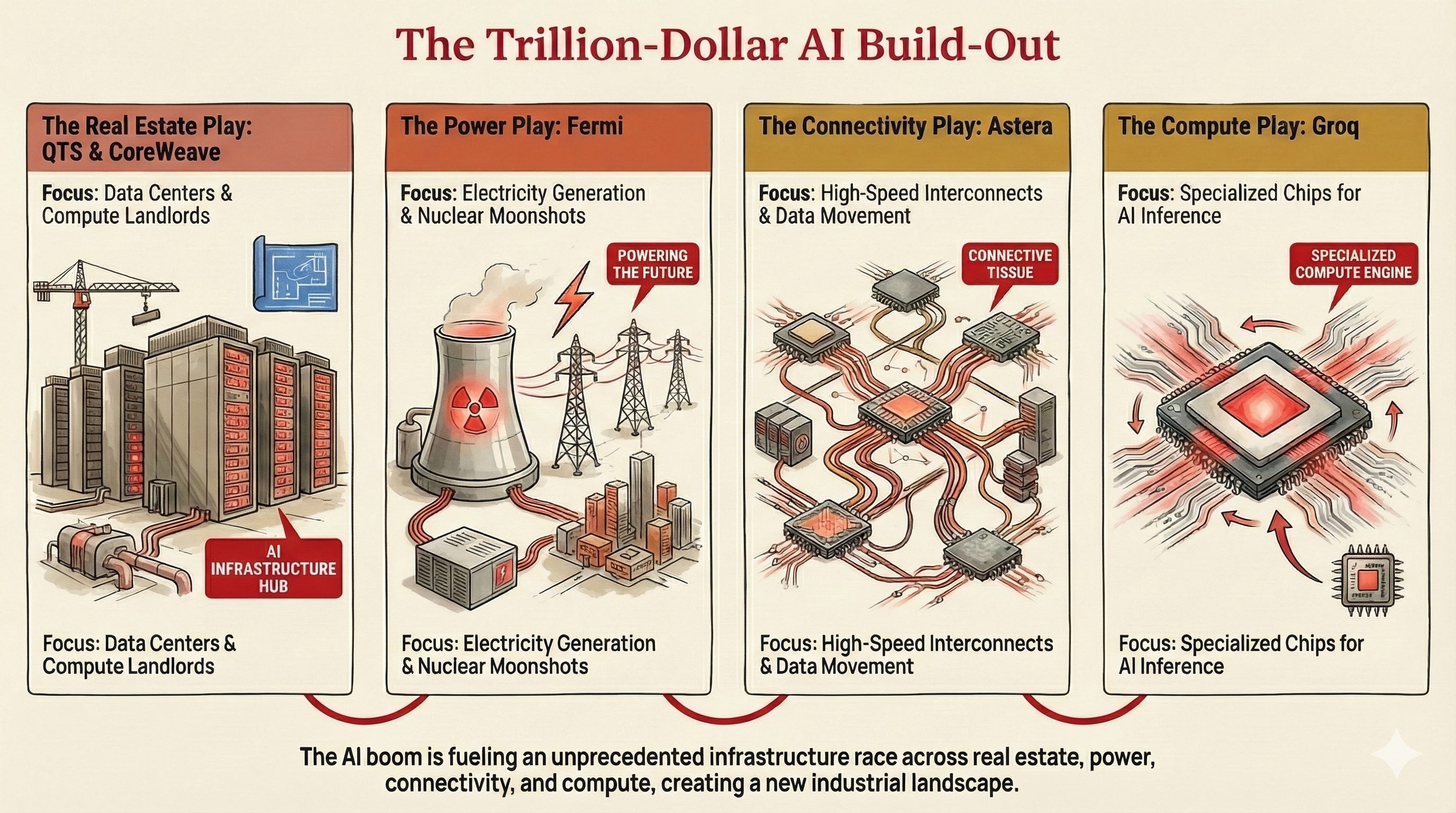

There are four major plays powering the AI boom:

The Real Estate Play: QTS and CoreWeave (physical infrastructure)

The Power Play: Fermi (the nuclear moonshot)

The Connectivity Play: Astera (the invisible infrastructure)

The Compute Play: Groq (specialized chips)

Since the beginning of 2025, these companies have seen their stocks surge and multiple executives become multi-billionaires. Even as doubt surrounds the AI bubble, fortunes are being made.

Here are their stories.

The Accidental GPU Barons: CoreWeave

Mike Intrator, Brian Venturo, and Brannin McBee were commodities traders at Natsource Asset Management. In 2017, they walked away from commodity trading jobs to try their hand at crypto mining, a side of the internet that still felt half-experiment, half-gamble. They bought GPUs online, stacked them wherever they could, and ran them hard.

When AI hit its inflection point in 2022, the pieces clicked. Everyone wanted GPUs. Very few could get them, power them, or house them fast enough.

CoreWeave’s pivot was simple. They became landlords for compute. They bought GPUs in bulk, put them where power was available, and rented access to anyone desperate enough to pay. For AI startups, it was faster than building their own infrastructure. For CoreWeave, it was a tollbooth.

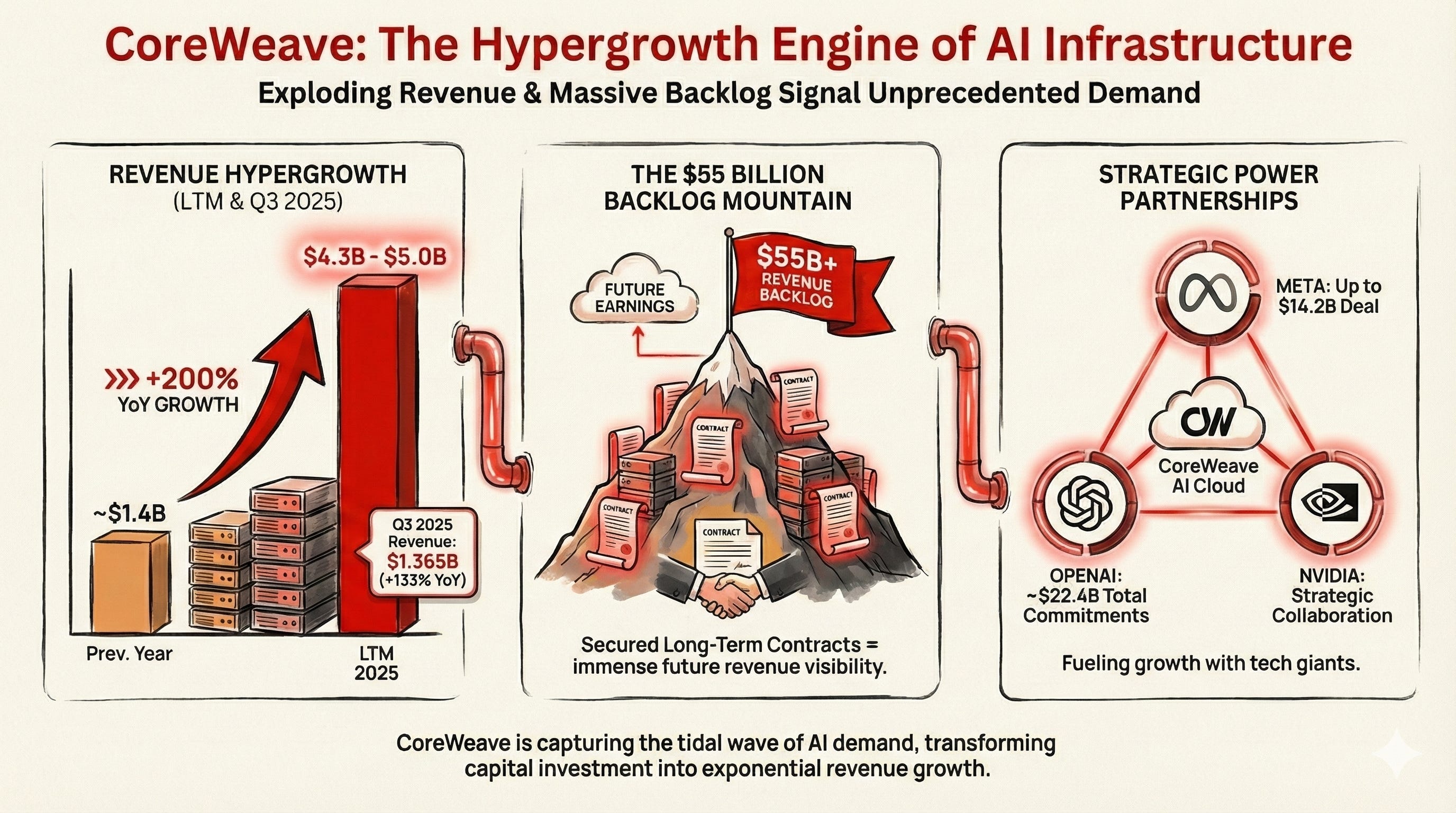

The business scaled quickly. Nvidia became both a supplier and an investor. So did Coatue. By 2023, CoreWeave was a unicorn. By early 2025, it went public, debuting at a $23 billion valuation, the largest US tech IPO in two years.

Today, CoreWeave runs dozens of data centers across the U.S. and Europe and controls hundreds of thousands of GPUs. Critics point to the circularity of the model: Nvidia funds companies that turn around and buy Nvidia chips, but the investors seem unbothered.

Since the IPO, CoreWeave’s stock has surged, and the three founders have quietly crossed into billionaire territory.

The Data Center Prophet: Chad Williams of QTS

Years before the AI boom, Chad Williams laid the groundwork for a data center empire.

In his early days, he ran his family’s car salvage company and soon ventured into real estate. In 2003, he and his wife Jeannie bought the office of a company that went bust during the dot-com boom. The building was unremarkable, except for one thing: it also housed a small but growing data center. Watching it operate up close gave Williams a quiet but powerful signal about where computing was headed.

That same year, he launched QTS, starting with the acquisition of a data center in Georgia. He was early, and he leaned into it. Over time, QTS snapped up unlikely assets: a former Chicago Sun-Times printing plant, an old semiconductor fabrication site outside Richmond, Virginia. Industrial leftovers, repurposed for a digital future.

General Atlantic invested in 2009. QTS went public four years later.

In 2021, Blackstone took QTS private in a $10 billion deal that saw Williams stay on as CEO. It became one of North America’s fastest growing data center landlords.

As AI companies scramble for facilities that can handle massive energy loads, QTS’s existing sites with power infrastructure are now worth far more than when Williams had built them. They’re renting access to electricity, which is now quickly becoming the bottleneck.

AI companies also need “hyperscale” facilities that have massive footprints with redundant power and cooling. QTS specializes in this. They’re likely signing long-term leases with AI companies at attractive rates.

But over time, disagreements bubbled up between Williams and Blackstone. This spring, Williams left QTS after Blackstone bought out his stake, walking away with about $3 billion. The Kansas billionaire recently announced he would be launching a new company, Quality Infratech Intelligence, to advise data center operators and other industrial businesses on their power infrastructure. Over time, it plans to build data centers too.

From car salvage to a $3 billion exit, Williams saw the future of computing infrastructure before almost anyone else.

The Nervous System Builders: Astera Labs

Early in his career, Sanjay Gajendra grew tired of building products that never made money. He developed a friendship with Jitendra Mohan, who kept winning patents that often brought money.

Both were engineers at Texas Instruments when they noticed something brewing in AI. As AI models grew larger, the real bottleneck would be connectivity. The pipes between GPUs would need to get much faster, much smarter.

When their employer, Texas Instruments wasn’t interested to pursue this idea, they decided to quit and start Astera Labs in 2017.

The company began in Gajendra’s garage in Santa Clara. Five years later, Astera had rolled out three core product lines spanning hardware and software, all focused on a problem few were paying attention to: moving data between processors fast enough to keep AI systems from choking. While the rest of the industry obsessed over GPUs and megawatts, Astera worked on the connective tissue in between.

Astera went public in 2024. Its valuation has since climbed roughly fourfold, to around $24 billion.

The Dropout Visionary: Jonathan Ross of Groq

In 2012, Jonathan Ross was working on ad systems at Google, and thinking about computer architecture on the side.

He wasn’t supposed to be there in the first place. Ross didn’t have a college degree or a high school diploma. Still, he found himself inside Google, close enough to see how machine learning workloads were starting to strain the hardware underneath them.

GPUs, built for gaming, were doing the heavy lifting. He felt like the wrong tool was being forced to do the right job.

Ross joined a small group inside Google that started asking an uncomfortable question: what if the chip itself was the problem? That line of thinking eventually became the TPU (tensor processing unit), a chip designed specifically for machine learning. Google kept it internal at first, using it quietly, letting it mature away from the spotlight and today, it has become its central hedge against NVIDIA.

By 2016, Ross and a few colleagues left Google and started Groq. Chamath’s Social Capital led a $10 million seed round.

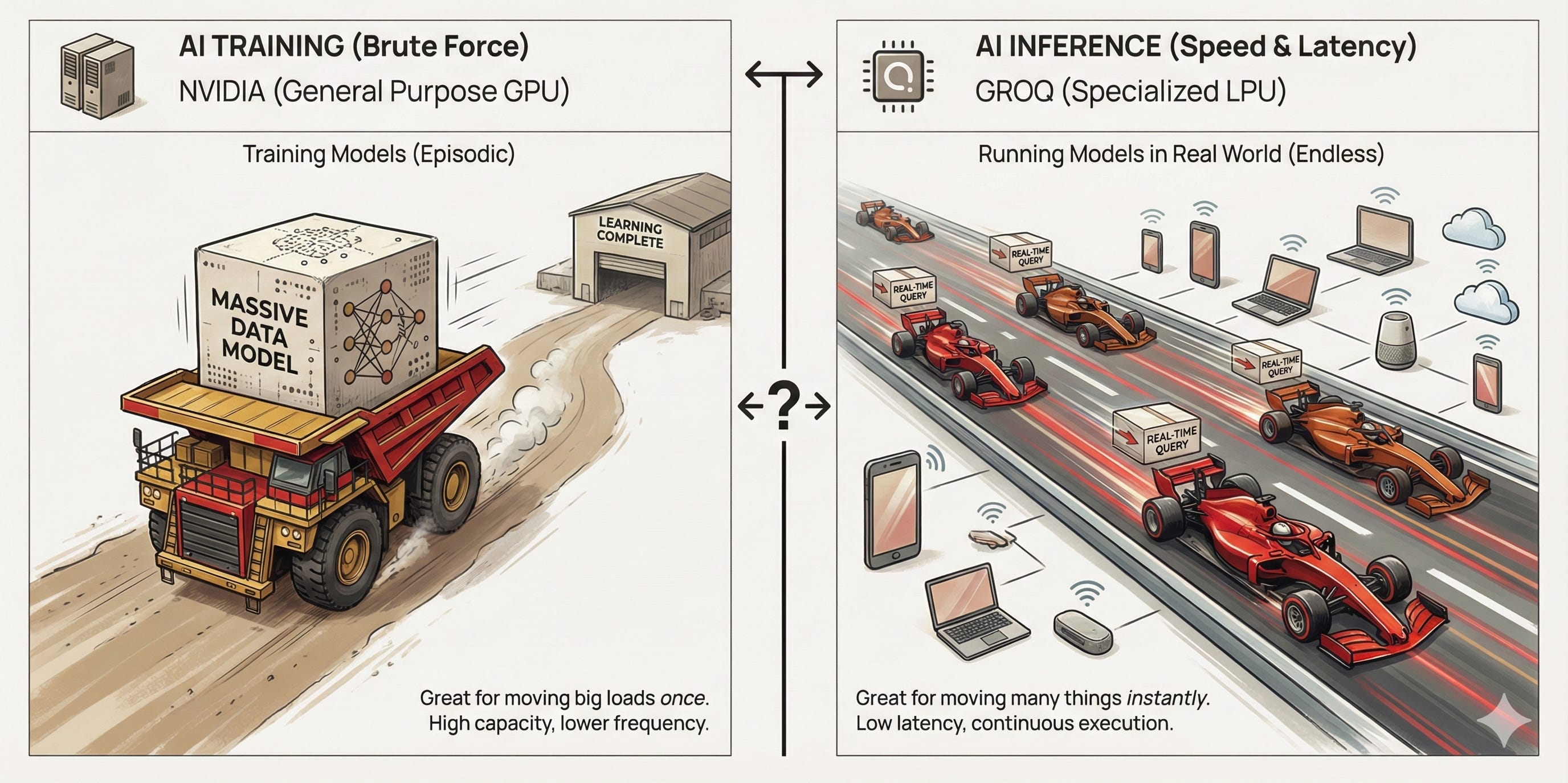

From the beginning, the bet was slightly counterintuitive. Groq wasn’t trying to win the training race. Training models was expensive, glamorous, and headline-worthy. But it was also episodic. The real cost, Ross believed, would show up later, when companies tried to run these models over and over again in the real world.

Groq built chips that were designed to run AI models fast, predictably, and cheaply. While everyone else talked about bigger clusters and more power, Groq focused on throughput, latency, and cost curves.

As AI moved out of demos and into production, companies began to feel the weight of inference costs. The thing Groq had been optimizing for suddenly mattered.

In September, Groq raised $750 million at a valuation of $6.9 billion, pulling in names like BlackRock and Cisco. The round had to be reopened because demand exceeded expectations.

Ross’s path has never followed the standard Silicon Valley arc. Neither has Groq’s. While much of the AI boom has been about brute force, Groq was built around a quieter insight: that the future of AI would have to be run locally, endlessly, and affordably.

That turns out to be the harder problem.

The Nuclear Moonshot: Fermi’s Bet on Tomorrow

Fermi Inc. is a data center company without a data center.

Its most tangible asset is a leased patch of land in Amarillo, Texas, still untouched. Yet the company’s valuation has surged on the promise of what it wants to build there: a self-contained, nuclear-powered AI compound in the Texas panhandle called Project Matador.

Fermi was cofounded by Toby Neugebauer, a serial entrepreneur, alongside former Texas Governor Rick Perry and his son, Griffin.

The plan is ambitious. Fermi says its 5,236-acre Amarillo site, which is touted to be an Advanced Energy and Intelligence Campus, will eventually host four Westinghouse nuclear reactors, with the first coming online in 2031. Until then, the company plans to rely on renewables and natural gas.

By 2038, Fermi claims the site will generate 11 gigawatts of power to support 15 million square feet of hyperscale AI data centers. To put that in perspective, one GW of power requires an estimated $10-15 billion of capital investment.

The scale is striking, especially for a company that is less than a year old. In a recent shareholder letter, Fermi described the project as “the Manhattan Project of our generation.”

Investors have responded. Fermi’s shares jumped 55% on the day of its upsized IPO in October.

Whether Project Matador becomes foundational infrastructure or a monument to excess is still an open question. But the bet is clear: nuclear power and AI are converging, and Fermi intends to be early.

The Question Nobody’s Asking

These fortunes represent something unprecedented: wealth being created not from the technology itself, but from the infrastructure that makes the technology possible. The picks and shovels.

The AI infrastructure boom is consuming $611 billion in capital with projections climbing every month. But here’s the uncomfortable question hanging over all of this: what happens if AI demand plateaus?

CoreWeave’s circular financing with Nvidia, Fermi’s valuation before building a single reactor, the unanimous analyst “buy” ratings on companies valued in the tens of billions: these are signs of either transformational vision or dangerous speculation.

History suggests caution. The railway boom created Vanderbilts and Carnegies. It also left investors with worthless bonds and tracks to nowhere. The fiber buildout of the late 1990s buried the ground in dark fiber that took decades to light up, if it ever did.

The difference this time is speed. Railways took decades. Fiber took years. The AI infrastructure race is being run in months. Whether that pace creates durable value or simply accelerates the crash is the bet being made, whether anyone admits it or not.

Sources:

This article comes at the perfect time; your take on the "picks and shovels" of AI being where the fortunes are made is briliantly incisive and a bit ironic. Does this mean the biggest innovation will soon be in grid infrastructure?